For most families, purchasing a home is one of their greatest dreams. However, banks look at your CIBIL score first when you apply for a loan. When you have a low score, it can feel like you’ve hit a brick wall because lenders may reject your application, demand a lot of paperwork, or charge high interest.

The fact is that having a low credit score does not mean you can’t get a home loan. You just need a good strategy, the appropriate lenders, and some smart financial moves. Even with lower credit scores you can purchase a home in 2025 with the help of multiple options availability which includes Government-backed housing programs and NBFCs.

What Counts as a Low CIBIL Score?

Credit score, also known as CIBIL, is a range of numbers between 300 and 900. This score represents how well you have handled your credit in the past. This score is also influenced by your card usage and your loan repayment history. So, by seeing this score lender will understand how financially disciplined you are.

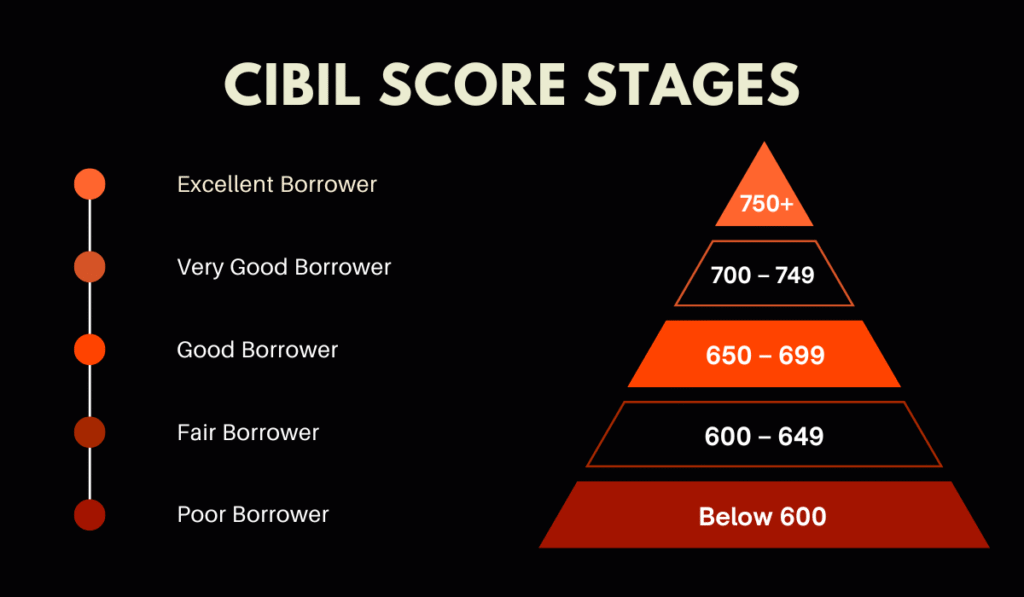

- If Your score is 750 or above then banks view you as a “Excellent” borrower. Why because this much score tell the lenders that your are financially disciplined. Banks provide good loan term to these borrowers because of there excellent financial history.

- Banks will treat you as a “Good” borrower when your CIBIL score lies between 700 to 749. In this range majority of banks are willing to grant loans, with fair loan terms. This score tells the bank that you are decent in financial decisions.

- If you are a borrower and your CIBIL score lies between 650 to 699. Then bank treat you as an “Average” category borrower because of your poor financial decision. Loans are still available, but the terms and interest might be very high. So in this case timely loan payment is important, because this range considered to be risky.

- Lenders view you as “Risky” borrower if your CIBIL score less then 650. At this stage bank hesitate to provide you loans, but NBSFC’s and other lenders might able to help you. If you try to improve your CIBIL score then only you get better loan terms in future.

The Difficulties of a Low CIBIL Score in Real Life

There are certain obstacles to getting a loan with a low credit score. You need to be prepared to face these difficulties:

- Lenders may ask for high interest rates because of more risk.

- Loan amount will be reduced, because at this stage lenders will not finance 80-90% cost of your house.

- Because of higher risk, lenders may ask for securities such as property collateral, guarantors, or co-applicants.

- Banks closely analyze your bank statement and your documentation.

The good news is that these difficulties are temporary. You can still get funding and negotiate better terms by playing smart.

Options to Get a Home Loan with a Low CIBIL Score

If your score is less than 700, don’t worry. You still have multiple routes to explore.

1. Apply with Housing Finance Companies or NBFCs

These companies are more flexible as compare to strict traditional banks. NBFC’s and Housing Finance Companies generally help the borrowers to get loan but the loan terms will depends of your CIBIL score.

Here are some NBFC’s and Housing Finance Companies : HDFC Ltd, LIC Housing Finance, and international equivalents like Quicken Loans or Rocket Mortgage. They accept applicants with scores as low as 600, though rates will be higher.

2. Add a strong credit Co-Applicant

If your CIBIL score is low, and you are facing difficulty to get loans. Then adding spouse, parent, or sibling with strong CIBIL score as a CO-Applicant will increase your chance to get loan.

3. Pay a Higher Down Payment

Imagine buying a house worth ₹50 lakh or $60,000. Normally, banks finance 80–85%, but with a low score, they may only give less. If you can pay 30–40% upfront, lenders see lower risk and are more willing to approve.

4. Use Property as Collateral

Facing problem in loan approval at low CIBIL score? In this case if you already own another property, you can opt for a Loan Against Property which is called LAP. Then lenders feel secured and they don’t worry about your CIBIL score.

5. Explore Government Schemes

For a secure and reliable home loan, you should opt for government housing schemes. Governments generally offer affordable housing schemes with relaxed eligibility.

Here are some good government financial schemes:

- In the US : Federal Housing Administration (FHA) Loan offer good loan terms

- In the UK: First Homes scheme provide good loan terms to first-time buyer’s.

- In the India: Pradhan Mantri Awas Yojana (PMAY) offers loans at a very low cost.

- Globally: Russia, Germany, and several other countries goverment have similar schemes.

More Than Your CIBIL Score Documents and Proofs Matter

If your CIBIL score is low and lenders are not providing good loan terms, you can still take a solid approach that is strong paperwork. This alone can work in your favour

What matters the most:

- At least 6–12 months of salary slips and bank statements

- Proof you have cleared old debts (no pending EMIs)

- 2–3 years of Income Tax Returns (ITR) – if self-employed

- Healthy transactions History – no overdrafts or bounced cheques

Tips to Improve Your Chances of Getting a Home Loan

Before applying, make your profile stronger. Some quick steps work like magic:

- Check your latest credit report and dispute errors if any.

- Clear pending EMIs or credit card bills immediately.

- Too many loan applications inquiries hurt your CIBIL score avoid them.

- Debt to income ratio need to below 40%.

- Applicants with low CIBIL score, choose lenders who offer pre-approval.

Loan Interest Rates You Can Expect in 2025

Here’s an approximate idea of the interest rates based on your score:

| CIBIL Score | Interest Rate (Annual) | Lender Type |

| 750+ | 8.25% to 8.75% | Banks/NBFCs |

| 700–749 | 8.75% to 9.5% | Banks/NBFCs |

| 650–699 | 9.5% to 11% | Mostly NBFCs |

| Below 650 | 11% to 14% | NBFCs/Private Lenders |

These are indicative rates. Always compare offers before signing up.

Myth-Busting: Low Score Home Loan Edition

Myth: Low CIBIL score means Loan rejection.

Fact: NBFCs, government schemes, and co-applicants make it possible, but you have to try harder.

Myth: Minimum 5 to 10 years will take to Improving your CIBIL score.

Fact: Clearing EMIs and maintaining healthy banking history even these small habits can improve your score within 6–12 months.

Myth: Only your CIBIL score matters.

Fact: Income stability and proper documents matter equally.

Things to Know Before Applying Home Loan with a Low CIBIL Score

- Low CIBIL score does not means doors are closed it only narrows your options.

- Even your CIBIL score is low government schemes, NBFCs and housing finance companies will help you.

- If you do these smart tricks like adding a co-applicant or paying a higher down payment increases approval chances.

- Present strong paperwork will definitely improve your chance for loan approval.

- If you start with higher interest rates, but you can refinance it later once your CIBIL score get improved.

Conclusion: Despite a Low Score, You Can Still Build Your Dream Home

You can turn your dream into reality, with the help of governments schemes because they are continuously pushing affordable housing loans, many lenders provide flexible loan terms and now new finance companies are expanding. With strong paperwork and good financial decision you can build your dream home.