Do you know around 60% of people struggle from saving money? In current conditions, with rising expenses and unexpected costs, budgeting is your key weapon to financial peace of mind. We hear this from every budgeting advisor – Learn how to budget. But no one actually explains what it really means. In reality, budgeting is about managing your money rather letting your money control you. It look straightforward, but when you think about it, it’s much more complex.

Basically, this guide breaks down budgeting into simple steps that anyone can understand regardless of age. By following these steps with consistently you’ll build a bright future. So, without wasting any time, let’s discuss the important steps

Important steps to learn how to budget

1. Track Every Expense

Before taking down your financial estimate ,you need to understand where you are spending your money unnecessarily for a month, note down every expenses no matter how small it is.

Useful Tips to track expenses:

- Use a notebook or budgeting apps like Mint or YNAB.

- Scrutinize your bank statement of last month.

- Start grouping expenses into categories like groceries, transport, entertainment.

Examining expenses makes hidden costs clear and helps highlighting unnecessary expenses.

2. Set Clear Financial Goals

Without purpose or any aim, budgeting feels like guesswork. Decide what you want to create from your saved money.

- Build emergency fund by cutting your 3 to 5 months unnecessary expenses.

- Start saving for a trip or a big purchase.

- Clear all your debt or start investing.

3. Differentiate Needs vs. Wants

Most easy way to save is through bifurcating needs (essentials like food, clothes ) and wants (non-essentials like eating out, subscriptions).

- Full fill your needs first.

- Control your wants without cutting all your funs and happiness.

For example, switching from cable TV to a single streaming service can save ₹1000+ monthly.

4. Choose a Budgeting Method That Helps You

Invest into a popular plan until you find out that plan which is favorable for your goals.

| Budget Method | Ideal For | How It Works |

| 50/30/20 Rule | Beginners | 50% needs, 30% wants, 20% savings or debts |

| 70/20/10 Rule | Balancing spending & saving | 70% spending, 20% savings/investing, 10% debt/donations |

| Envelope System | Trouble controlling spending | Cash envelopes for each category; stop spending when empty |

| Zero-Based Budget | Detailed planners | Assign every rupee a job; income minus expenses = zero |

For beginners, the 50/30/20 rule is a great option to start because of its simplicity.

5. Build an Emergency Fund

Life is full of unexpected turns ,be prepared for it by saving your money.

- Try to save at least 3-6 months of expenses.

- Turn on automatic transfer of these funds even if it’s a ₹500/month.

- Use this savings for extreme emergencies.

6. Automate Your Savings

Using automated payment transfer system to auto transfer your monthly saving to your saving account this will make your saving effortless and more consistent.

7. Cut Back on Wasteful Spending

Look closely at your day to day life.

- Cancel subscription of unused apps.

- Stop online shopping’s to prevent delivery charges.

I saved almost around ₹10,000/month by no longer buying lunch outside, cooking at home, and cutting out unnecessary app subscriptions.

8. Use Budgeting Tools and Apps

Modern days tools can help you in budgeting.

- Use online app like : Mint, YNAB, or Wallet to observing your spending.

- Set reminders for bill payments to escape due charges.

- Digitally see where you can save more.

Use a tool that feels easy to understand and continue with it.

9. Plan for Inflation and Rising Costs

Inflation means sustained increase in the price of your valuable over time. Add a 3-5% buffer in your budget to cover rising prices on things like : groceries, fuel, and utilities.

10. Review and Adjust

Budgeting is a living process:

- Review your budget to prevent extra expense.

- Cherish your small amount of savings

- Adjust your savings based on your goals and aims.

This is how you can achieve your goals, be economical.

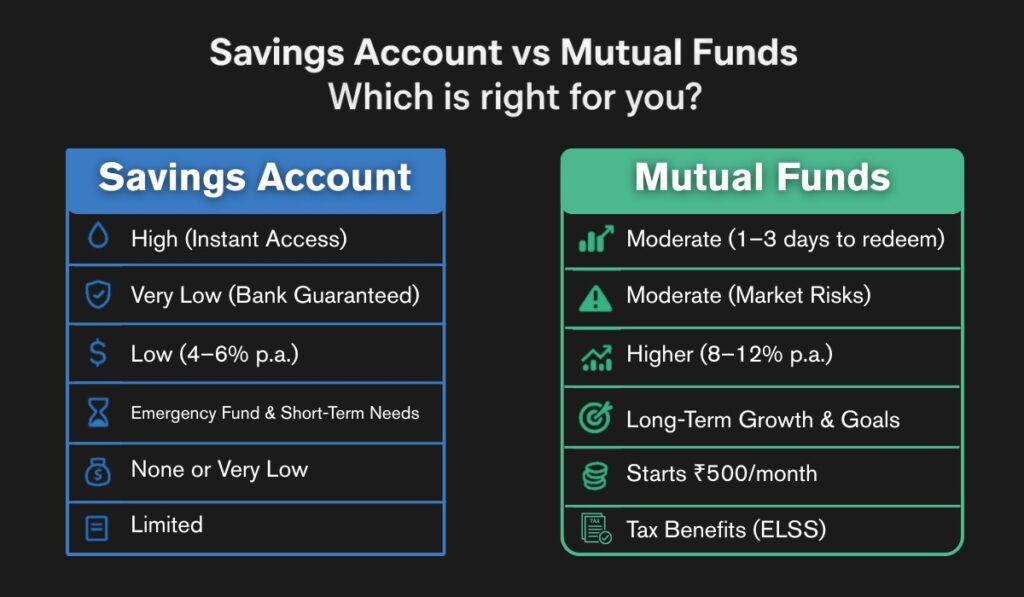

Savings Accounts vs. Mutual Funds: Where Should You Save?

Here’s a quick comparison ,which help you to make up your mind where to invest.

| Feature | Savings Account | Mutual Funds |

| Liquidity | High (instant access) | Moderate (1-3 days to redeem) |

| Risk Level | Very low (bank guaranteed) | Moderate (market risks involve) |

| Returns | Low (around 4-6% p.a.) | Higher (8-12% p.a. average) |

| Ideal For | Emergency fund & short-term needs | Long-term growth & goals |

| Minimum Investment | None or very low | Starts around ₹500/month |

| Tax Benefits | Limited | Tax benefits under ELSS schemes |

Conclusion

Budgeting is a step which leads you to financial stability .Start with analyzing your expenditure this month. Try the 50/30/20 rule. Establish your emergency fund with ₹500/month. Stop spending on unnecessary things and watch savings grow rapidly.

Don’t think too much just start learn how to budget will give you lot of stability in your life. Remember, you don’t have to earn lakhs to save vast quantity of money — even small, consistent steps matter.

Your writing is a true testament to your expertise and dedication to your craft. I’m continually impressed by the depth of your knowledge and the clarity of your explanations. Keep up the phenomenal work!