Investors Are Holding Cash: Unveil the reasons why cash is king in 2025 with expert tips for beginners, myths debunking, and sensible strategies for holding cash in a volatile market. The year 2025 has brought new uncertainties to the financial markets that smart investors decided to put their strategies on hold and rethink them.

In the midst of these extreme fluctuations of stocks, real estate, and crypto, one refuge has come back to the forefront cash. What can beginners take from this to safeguard and build their wealth? Keep reading to discover that having cash on hand is not just “doing nothing”, but rather a tactical move that can secure your success.

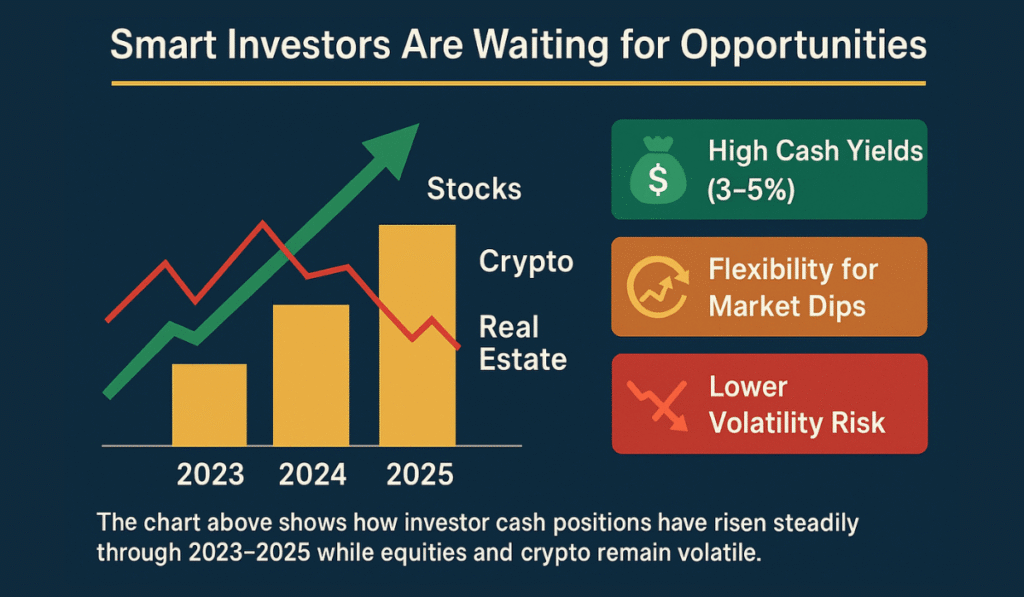

What Smart Investors Are Holding Cash & What Are They Doing with Their Money

Attractive Returns & Lower Volatility

Interest rates are still above their very low levels of the past years, thus cash and money market funds being much more rewarding than in the previous years. Even if rate cuts are expected, cash yields are still positioned to be competitive in 2025 and with almost zero volatility it’s a safe investment against uncertain markets.

Flexibility for New Investment Opportunities

Markets are very dynamic. When stock prices fall or new investment opportunities appear—a sudden real estate deal, a significant market correction, or a promising IPO—people with cash in hand can make their moves fast, thus buying assets at their lowest.

Emergency Buffer

Life is full of surprises. Medical emergencies, job loss, or a sudden expense can take even the most robust financial plan by surprise. Financial specialists advise to always hold enough cash for the nearest spending needs, be it tuition fees or big purchases. It’s not an excess; it’s your safety net.

How and Why You Should Keep Some Cash

1. Be Aware of Different Ways to Handle Your Cash

- Savings Accounts: Nowadays, a high-yield online savings account offers up to 5% of interest—this is still quite low but significantly better than the typical bank rates of the past.

- Short-term Government Bonds: “Treasury funds” can be considered safe places to keep your money, as they are always dependable.

- Money Market Funds: These are very conservative investments that give you the chance to have your money at hand and also make a little more than in a savings account.

2. Situations when It Is Good to Keep Money in Cash

- You see that stocks will go down or that they will become very unpredictable.

- You will need money quite soon (maybe during the next 1–2 years).

- You are looking for a good moment to enter the market/a “deal” which is a way to invest with less risk.

3. How Much Money Should You Keep in Cash?

- Generally, six to twelve months of living expenses should be kept as cash, suggests the majority of the experts. In the case of the stock market, it only depends on the risk tolerance levels whereby some individuals decide to keep 5-20% of their portfolio as liquid assets whereas others may have a higher figure during periods of high volatility.

Common Myths About Holding Cash

Myth 1: “Cash Means Lost Returns.”

- It is not necessarily so that holding cash means missing out. In the long run, cash cannot compete with stocks, but it is the latter that lose value in volatile or falling market situations. In such cases, having cash on hand allows one to avoid losses and have the power to buy assets at bargain prices.

Myth 2: “Only Risk-Averse Investors Hold Cash.”

- It is not correct! Some of the wisest investors—like Warren Buffett—have actually been holding large amounts of cash lately in order to be ready for the next big opportunity. The aim is not to completely avoid risk but to achieve a balanced portfolio.

Myth 3: “Cash is Useless During Inflation.”

- It is a fact that cash loses its value during inflation, but if one is to use it strategically—such as by keeping only what is necessary for emergencies and short-term spending—then the negative side of it can be alleviated, and the rest of the money can still be invested for growth.

General Feedback :

— Investing @ Prakash (@Prakashplutus) March 16, 2024

Many big guys are still sitting with 20% + cash in hand , they are holding 20% cash levels from many months , so far they have gone wrong .

I hope you understand this , God bless all

Actionable Steps for Beginners

- Start with defining your goal: Figure out the amount of money you’d require to cover your living expenses for 6 to 12 months in case of an emergency.

- Pick the suitable account: Place your money in a cash reserve through high-yield savings or money market accounts.

- Don’t put all your eggs in one basket: Don’t move all your investments to cash. Keep a mix of stocks, bonds, mutual funds, and other securities.

- Dollar-cost averaging: Employ cash to slowly acquire assets over time rather than taking the risk of large sums in a single market fluctuation.

- Check up on your plan often: Remember to tweak your cash reserves according to your personal situation—new job, kids, purchases, investments.

Comparison Table: Cash vs. Other Investments

| Feature | Cash / Money Market | Bonds | Stocks |

| Safety | High (low risk) | Moderate (market risk) | Low (high volatility) |

| Yield (2025) | Competitive (3%+) | Varies (potentially higher) | Highest long-term, but variable |

| Liquidity | Instant access | Varies by maturity | High (can sell quickly) |

| Inflation Protection | Weak (loses ground) | Some inflation protection | Strong (beats inflation long-term) |

| Opportunity Cost | May miss growth | May miss best returns | Risk of larger short-term loss |

| Best Use | Emergencies, ready cash | Diversification, stable income | Growth, long-term wealth |

Real-Life Example

Let me introduce Priya to you, a young working professional. She had initially put aside 5 lakhs and placed it in a high-yield money market fund thus earning over 3% interest on the deposit. When the markets tumbled abruptly, Priya was able to buy quality stocks at a lower price, she thus accelerated the growth of her investment portfolio.

Her cash buffer was her source of courage to take action and at the same time, it was her shield during the period of job uncertainty — no selling out in a hurry, just making the right moves.

Tips: Best Practices for Holding Cash

- Define first a cash target which is relative to your monthly expenses.

- Do not fall into the trap of holding too much cash, as it can quietly lead to loss of your wealth because of inflation.

- Start saving automatically for your cash reserves via your bank or investment platform.

- Invest in money market funds if you have short-term goals; these funds offer better yields than savings accounts.

- When the markets are steady again, use the money that you had taken out of the investments to buy back in.

FAQ’s

Q1. How much cash should I carry in 2025?

Ans: Most financial advisors suggest 6-12 months of living expenses to be kept on hand for emergencies and you should personalize this amount.

Q2. Are money market funds a safe investment?

Ans: They provide a low-risk profile and stable returns. Money market funds are a good choice in 2025 if you are looking for safety combined with relatively high returns.

Q3. Will keeping money in cash reduce my returns?

Ans: In the short-term, cash is a safe haven; over time, stocks and bonds generate higher returns than inflation and create wealth. Find the right balance.

Q4. What risks accompany holding cash?

Ans: Inflation reducing the purchasing power is the major risk. It is advisable to use cash for liquidity and unplanned expenses only.

Conclusion

With markets being volatile as they are today, holding cash is not only for those who are extremely risk-averse but also it is a sign of an investor who is ready and flexible. Keep cash as a tactical cushion that is always available to you in case of emergencies or to make new investments in 2025.

Take stock of what you have, set a target, and continue with your financial plan because sometimes the smartest thing to do is to be prepared for anything.